Ixsight is looking for passionate individuals to join our team. Learn more

Ixsight is looking for passionate individuals to join our team. Learn more

With the constantly changing environment of financial compliance, Anti-Money Laundering (AML) transaction monitoring has become a key defense against financial crime. Modern AML software plays a critical role in helping financial institutions detect suspicious activities and prevent money laundering. As global financial systems become more interconnected and digital transactions increase, the need for advanced AML transaction monitoring solutions continues to grow.

AML transaction monitoring works by examining customer transactions to identify unusual patterns that may indicate money laundering, terrorist financing, or other financial crimes. Financial institutions rely on intelligent AML software to analyze transaction data, reduce false positives, and support compliance teams in detecting risks more efficiently. As regulations become stricter worldwide, organizations face increasing pressure to strengthen their payment transaction monitoring capabilities and adopt more advanced compliance technologies.

This effort is based on the AML Transaction Monitoring Process. It starts with the gathering of data, where data on transactions in terms of amounts, frequency, origin, and destination is collected through different sources. Risk assessment then gives scores according to the profile of customers, historical behavior, and external risks such as geographic risks. Robots are then used to identify anomalies by using rules and algorithms, and compliance teams then investigate them. In case of a suspicion, we report to the authorities, which in the case of the US are Suspicious Activity Reports (SARs). This cycle provides a continuous vigilance, but the conventional approaches tend to be overly high in false positives and manual workload.

The future state of transaction monitoring concerning AML in 2026 is going to be revolutionized with the application of artificial intelligence (AI), machine learning (ML), blockchain integration, and real-time analytics. These developments will ensure AML software is more effective, cost-effective, and yet more accurate. As an example, AI-based applications are able to process massive data sets in real-time to anticipate risks before they become real. Monitoring of payment transactions, specifically, will experience changes towards behavioral analytics, shedding off their inflexible system based on rules to one that adapts to patterns.

To further elaborate, the blog examines the AML Transaction Monitoring Process, including the latest trends and challenges, and the most preferred AML software to monitor transactions in the year 2026. No matter which side of the coin you are, be it a compliance officer, fintech innovator, or regulator, it is important to learn about these developments in order to be ahead of the curve in the war against financial crime.

AML Transaction Monitoring Process is a methodical mechanism that aims at detecting and reducing the risks related to money laundering. Primarily, it is the process of constant monitoring of financial transactions to make sure that they are not violating such laws as the Bank Secrecy Act (BSA) of the US or the Anti-Money Laundering Directives of the EU.

Step one: Data Aggregation. Institutions retain all details about transactions, such as wire transfers, deposits, withdrawals, and any digital payments. This is complemented with the customer information acquired by means of Know Your Customer (KYC) services, including identity check and risk classification.

Step two: Application of Rules and Generation of Alerts. With AML software, there is the application of predefined rules or scenarios. As an illustration, a regulation may identify the transactions made above a specific limit by the high-risk jurisdictions. Further systems include ML to identify minor anomalies, such as abnormal velocity in fund flows.

Action three: Investigation and Disposition. Analysts are then looking at flagged alerts and obtaining further context, whether it is a transaction history or external intelligence. In case of suspicion, a SAR is filed, the alert is closed, and audited.

Step four: Reporting and Feedback Loop. Deploying compliance teams gives feedback on the discovery to regulators, and insights are used to adjust the rules to minimize false positives in the future. This process is very important to ensure effectiveness is achieved.

This process is further performed in payment transaction monitoring, in which delays can be expensive in case of cross-border payment checks in real-time. There are data silos, a changing criminal strategy, and difficulties, but automation is used to scale operations.

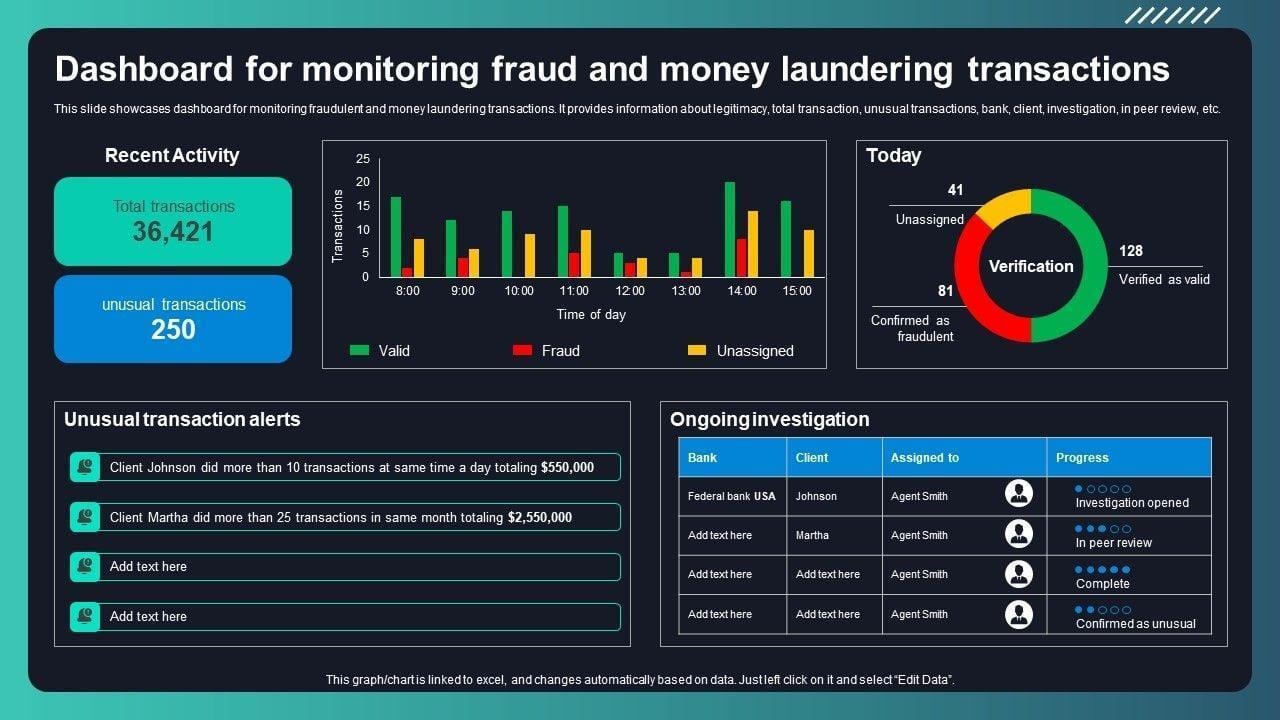

Implementation of the AML Transaction Monitoring Dashboard For Monitoring.

In the above picture, a standard AML transaction monitoring software dashboard is displayed, with live alerts, risk score, and transaction visualization helping to make rapid decisions.

In general, it can be concluded that the development of this process cannot be achieved without the combination of technology and human knowledge, which preconditions further innovations.

More: What is the AML Transaction Monitoring Process? How Does It Work?

There are a number of major trends that will form the future of transaction monitoring in AML by 2026 as a result of the impact of technology developments and regulatory trends.

First, AI and ML Integration. The monitoring will be dominated by AI-assisted monitoring to predict risks. As an illustration, they will screen the network analysis and behavioral biometrics to identify organized laundering operations. In payment transaction monitoring, AI would be able to handle millions of transactions per second and identify fraud in real-time, as well as cut down false positives by more than 70 percent.

Second, Instant and Real-Time Payments Monitoring. As instant payment technologies, such as the FedNow system, become popular, surveillance has to be performed within milliseconds. The trends are pointing towards the in-flow interdiction, where high-risk transactions are blocked prior to settlement. This will be essential to crypto and stablecoin transactions, in which volatility complicates matters.

Third, Cryptocurrency and Cryptocurrency Loyalty. Due to the increased virtual assets, AML software will be able to integrate on-chain analytics to trace funds across blockchains. Clusters of wallets and smart contract interpersonal communications will be tracked using tools that will identify illicit patterns. By 2026, new regulations, such as the proposals of the FDIC regarding stablecoins, will require more powerful KYT (Know Your Transaction) protocols.

Fourth, Collaborative Intelligence. The analytics that will be based on a consortium will also aid in the identification of cross-border threats since institutions will be anonymized to share data. This tendency is in line with the FATF recommendations on the partnership between the public and the private.

Fifth, Regulatory Tech( RegTech) Evolution. Simplified regulations that focus on the end results and not the process are to be expected, and AI can be used in compliance audits. Stiffer AML implementation in Europe and APAC will do the same in the implementation of adaptive systems.

Sixth, Fraud Typology Expansion. New threats, such as the use of AI-generated deepfakes and authorized push payment (APP) fraud, will be handled through monitoring. The use of behavior-based approaches will substitute the rules that will become ineffective as the typologies will change, and ML will be used to do so.

Seventh, Sustainably and Ethically Smart AI. With the evolution of AML software, attention will be paid to ethical AI, which provides transparency and impartial decisions to comply with ethics requirements in regulations.

Eighth, Integration with the Bigger Ecosystems. KYC, sanctions screening, and fraud prevention will be linked to transaction monitoring to have a comprehensive perspective.

These tendencies are indicators of change towards proactive over reactive monitoring, which enables institutions to fight financial crime more efficiently.

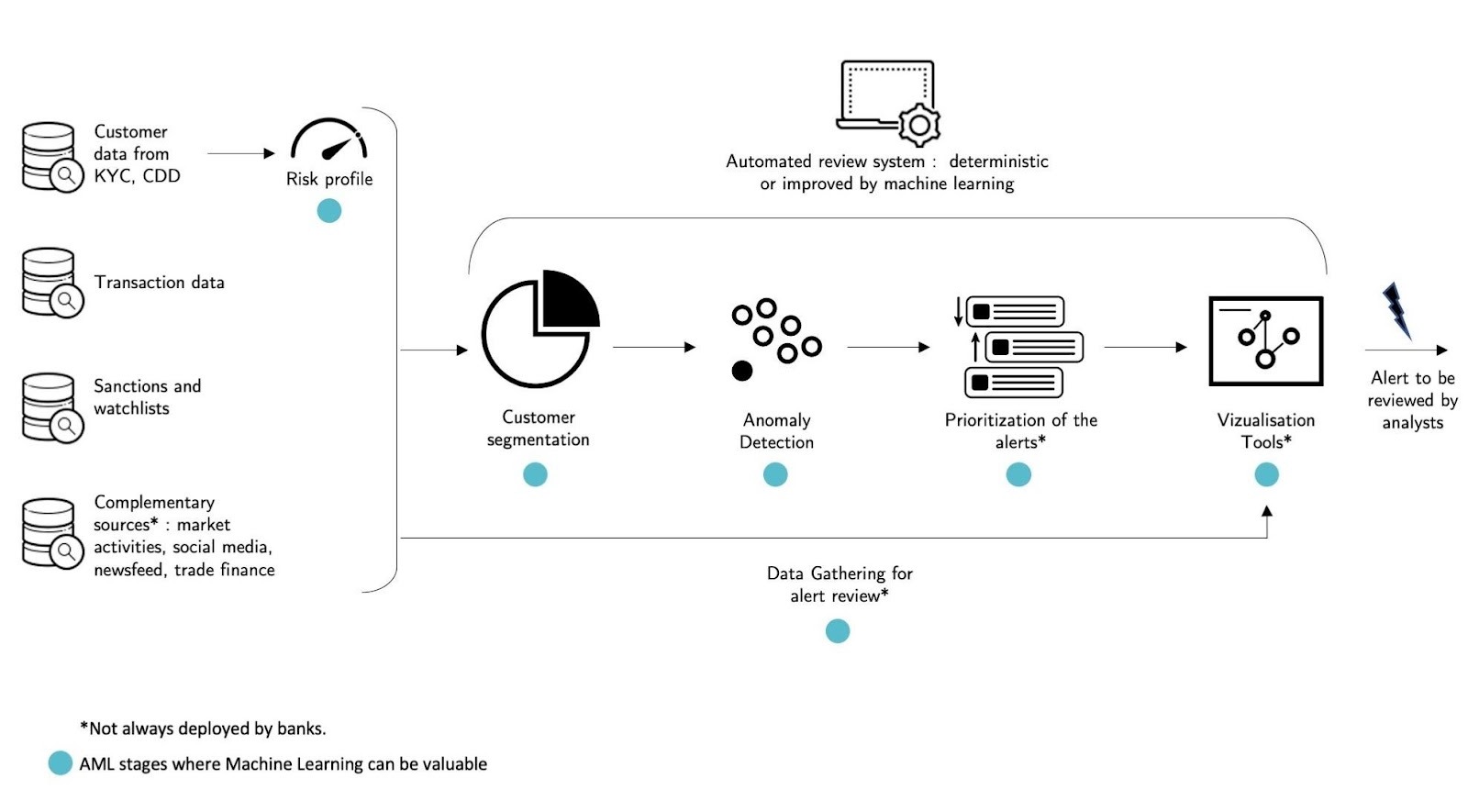

The Age of Artificial Intelligence Compliance with AML.

The above visualization shows how AI will be applied in the future in the context of AML transaction monitoring, with a focus on predictive and data integration capabilities.

In 2026, the best AML software to use in monitoring transactions will depend on how well they are scaled, include AI capabilities, and are compliant. According to market analyses, the following are the best competitors:

| Software | Key Features | Best For | Pricing Model | Strengths |

| ixsight | AI-powered AML transaction monitoring, real-time risk detection, automated compliance workflows, integrated KYC and sanctions screening. | Banks, fintechs, and financial institutions. | Custom enterprise pricing. | Advanced analytics, scalable platform, strong compliance automation. |

| Alessa | Real-time detection, AI-driven false positive reduction, unified AML platform with KYC and sanctions screening. | Financial institutions, fintechs, MSBs. | Subscription-based, scalable. | Top-ranked for analytics innovation and cost-efficiency. |

| ComplyAdvantage | AI-powered screening, dynamic risk signals, transaction monitoring with up to 70% false positive reduction. | Banks, fintechs, payment firms. | Tiered pricing. | Excellent for real-time monitoring and adverse media integration. |

| NICE Actimize | Enterprise-scale detection, behavioral analytics, and a holistic financial crime suite. | Large banks, global organizations. | Custom enterprise licensing. | Strong in complex environments with crypto monitoring. |

| Facctum | Cloud-native, low-latency monitoring for real-time payments, behavioral analysis. | High-volume institutions, cross-border payments. | Usage-based. | Ideal for instant decisions and audit trails. |

| SymphonyAI | AI-focused, global coverage, transaction, and negative media screening. | Worldwide banks. | Enterprise subscription. | Leader in AI innovation for risk detection. |

| Flagright | AI-native, real-time transaction monitoring, centralized detection. | Financial institutions. | Flexible plans. | High user ratings for ease of use. |

| SAS AML | End-to-end solutions, advanced analytics, and watchlist screening. | Enterprises need comprehensive suites. | Custom. | Proven in fraud and AML integration. |

These technologies are the next generation of AML transaction monitoring programs with a focus on AI to manage the needs of 2026.

Although the prospects of AML transaction monitoring in 2026 are bright with AI, machine learning, and real-time analytics, some of the existing challenges continue to jeopardize the progress, especially in smaller institutions and where the threats are rapidly changing. Meanwhile, these obstacles offer significant innovations, teamwork, and efficiency benefits. These are discussed below.

Current anti-money laundering (AML) techniques violate fundamental ...

This example shows the conflict of privacy in AI-based AML, which highlights the necessity of handling data ethically.

Breaking down the Barrier of Operational Efficiencies in an AML ....

The graph above points out the areas of inefficiency in operations, such as false positive overload in AML systems.

The other chronic challenges are huge amounts of transaction volumes, the absence of risk-based scenario tuning, and the complexity of regulations that tend to over- or under-monitor.

Nonetheless, 2026 will provide revolutionary possibilities as a solution to these challenges by becoming innovative and collaborative.

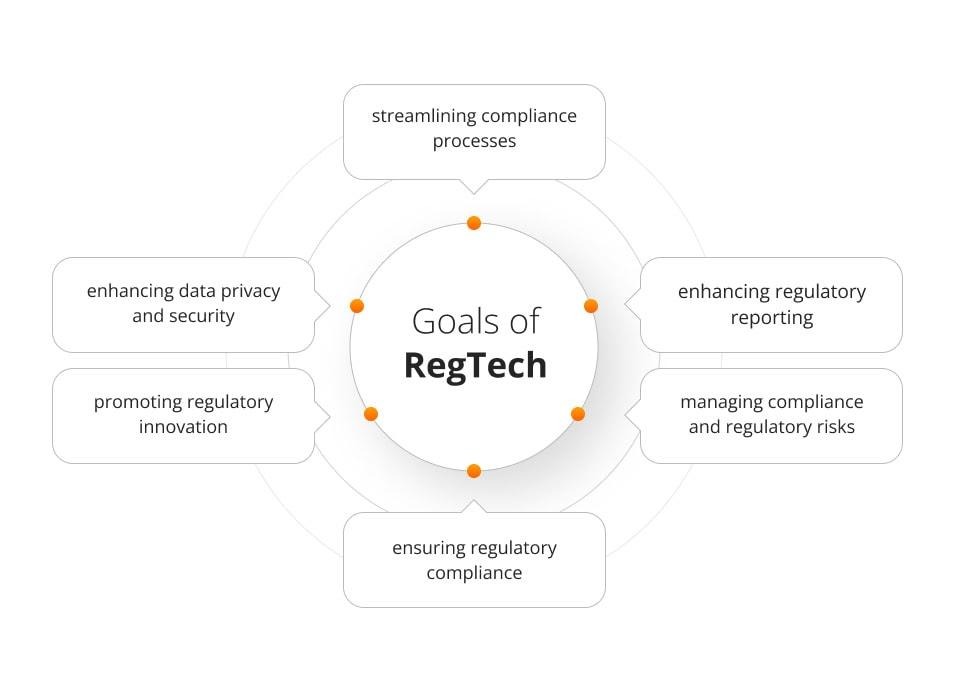

RegTech: How technology is changing compliance?

This diagram illustrates RegTech goals, emphasizing collaborative efficiency gains.

Also read: How to Identify & Report Suspicious Activities in Banking

The perspectives of transaction monitoring as a means of AML in 2026 are promising, and AI and real-time systems transform the sphere. The best AML software improves compliance and security since, by being aware of the AML Transaction Monitoring Process and implementing the best AML software, the institutions can improve compliance and security. With payment transactions monitoring taking a new dimension, the winning battle against financial crime will be proactive.

To support organizations in maintaining compliance and data integrity, Ixsight offers Deduplication Software, Sanctions Screening Software, Data Cleaning Software, and Data Scrubbing Software. These solutions help businesses streamline data management, detect anomalies, and ensure accurate customer verification, ultimately strengthening KYC and AML processes.

Our team is ready to help you 24×7. Get in touch with us now!